Author: Sarah Artist MPubPol, BAppSc(EAM), Dip PA (WAPPA)

Practice Lead Capability & Performance

The NSW Auditor General released his Local Government 2024 report in March this year, and it highlighted some of the financial vulnerabilities that we know exist within the sector.

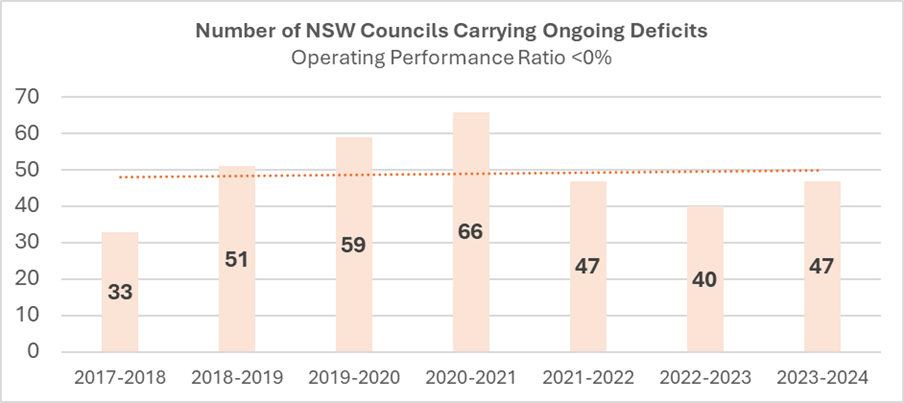

One of the key financial benchmarks used to track council performance by the NSW Auditor General and the NSW Office of Local Government is the operating performance ratio. This ratio provides an indication of whether the Council is carrying ongoing deficits, and the benchmark is a break even average over three years.

The number of NSW Councils that are falling below the benchmark in 2023-2024 was 47 out of a total of 128 Councils. This number peaked during Covid but has been gradually trending upwards from the 2017 results at which time there were 33 Councils failing the benchmark:

Figure 1- Source: NSW OLG Comparative Data

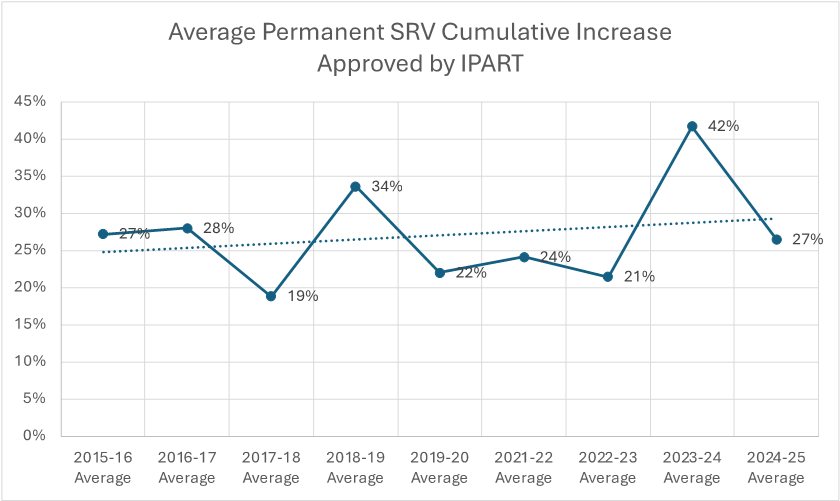

One of the ways that Councils can address underlying financial sustainability issues is to increase their income levels through a Special Rate Variation.

While there is a wide variation in the amounts sought by Councils in an SRV application, the average cumulative percentage increase approved by IPART has been growing since 2015 from around 25% to around 30%:

Financial Analysis in Service Reviews

The NSW government has now published an intention to review the SRV process, introducing a new process for IPART to conduct a ‘Comprehensive Spending Review’ of Councils wanting a permanent increase in rates.

Service reviews are a crucial process to address financial sustainability pressures, as they enable Councils to design, implement and demonstrate productivity improvements and cost containment strategies.

A thorough assessment of the financial performance of the service can assist your Council in making decisions and planning improvements, and with this information at hand you can present better projections and cost estimates for your service improvement plan.

A financial sustainability agenda can be built into each review, and here are some ways to ensure that this is comprehensively addressed:

Alternate service delivery models require more complex calculations and research in order to generate profit and loss estimates, and to inform Council decisions.

Only then, can you identify and plan improvements, and consider future cost implications. A future business-as-usual budget and resourcing model can then be developed once your improvements have been implemented.

The Centium Service Review team offers robust and proven management services specifically tailored to NSW local government. We work in partnership with our Council clients to build internal capacity and engagement with our process and outcomes.

Please reach out if you would like to talk to us about our Service Reviews – we can assist you to analyse your service, find efficiencies and new revenue, improve your systems and processes, and maximise your service delivery outcomes.

Visit the Centium website to learn more about our service reviews for local government: https://centium.com.au/services/risk-assurance-management/service-reviews/